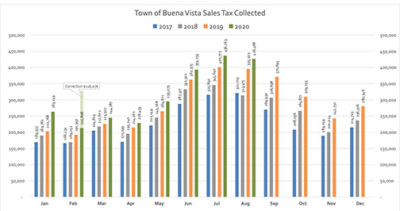

Buena Vista continued its solid run on summer sales tax numbers, with August figures almost eight percent higher than those of August 2019.

Stats going back to 2017 present the strong summer sales tax performance for Buena Vista, despite the challenges of COVID-19.

In addition, totals for the year through August are nearly 16 percent higher, according to Town Treasurer Michelle Stoke, who reported the figures to the BV Board of Trustees Tuesday evening.

With the strong summer figures, the current budget surplus stands at $199,125.

In all, the town took in $426,488 for August — $30,985 higher than August of 2019. Year to date tracking shows sales tax $358,078 higher than 2019, accounting for a rough spring during COVID-19 shutdowns.

It remains to be seen how the colder months and the COVID-19 landscape will play out for brick-and-mortar businesses as they seek ways to accommodate customers indoors.

Remote sales continue to represent a growing and significant portion of Buena Vista sales tax collections. In August, 13 percent of sales were from remote transactions.

While the total numbers are good for the town, the trend continues where a significant portion of the collected tax comes from remote sales. In August, for example, 87 percent of the collections were locally derived and 13 percent were remote.

A remote seller relates to businesses that make sales to someone who lives in Buena Vista, but the seller doesn’t have a physical presence in town. For example, if someone orders something from Home Depot online, and because there isn’t a Home Depot in Buena Vista, Home Depot is required to collect and remit sales taxes to the town when it is shipped here.

The remote seller issue came about in 2018; in the case of Wayfair v South Dakota, the Supreme Court ruling that sales tax must be remitted to the taxing jurisdiction of the purchaser in the case of online purchases. In response, Colorado passed legislation that said a remote seller was an entity that did not have a “brick and mortar” store in Colorado and was required to remit sales tax to Colorado.

Recent Comments